AI is quietly dissolving the walls between company functions. Sales can write product specs. Developers speak fluent “commercial-ese.” Everyone’s more empowered, more informed, more capable. So who’s actually steering the ship?

A thought piece by a product peer1 fueled my thinking here. They describe scenarios where the decision owner is fuzzy and product debt quietly builds up, often without anyone realizing it.

Winding back a notch, my interpretation of coherence is how you get a company aligned behind a mission, with everyone pulling in the same direction.

Pre-AI, the product function was key to leading that coherence – specifically owning product-market fit and managing the interactions between the business and engineering functions. In the AI era – certainly in tech-driven companies – those functions are no longer as siloed as they used to be.

The sales function is no longer purely commercial. They’re increasingly proficient at shaping their ideas, creating business requirement documents and doing a lot of the work (at least on the face of it) that a product manager or CPO used to. I’m no longer getting one-sentence ideas and a screenshot, but thought-out requirements and case studies as a starting point.

The same is happening on the engineering side. Developers are more capable of understanding how the business operates and speaking in a way that’s coherent to the commercial side. AI is powering this mutual understanding the same way real-time translation broke down language barriers.

Probably – in both cases – new hires will be increasingly geared towards those personality types as well, accelerating the trend. So, we have less siloed functions and people much closer together in the stories they’re telling. Everyone feels more informed, better educated, and more empowered to contribute to overall strategy.

But, if everyone’s a peer, two questions emerge: Who drives the unified mission? And what does the product function do in that world?

In my current role, this broader shift met a specific moment. We had moved through earlier phases – getting the tech stack scalable, then nailing product-market fit – and were beginning to scale toward enterprise partnerships. That scaling exposed something our existing model couldn’t absorb: end-to-end accountability for the customer and partner experience was diffused across teams, and what worked at current scale would break at enterprise volumes.

A product leader has always been a bridge between functions, but in advisory or facilitating modes. What changed was the shift from coordinating decisions to owning them – from consensus to single-threaded accountability. Nearly a decade of leading product had given me context across commercial, engineering, risk and finance, so I moved to work directly with our CRO on customer experience and partnership readiness as our core operating priority.

My new mandate: optimize every decision for quality revenue and customer experience.

To accelerate that goal, I embedded myself across the full customer journey – the operational UX, the internal metrics, the competitive landscape. Not curated summaries passed up from customer-facing leads, but direct exposure to every friction and dropoff, so the trade-offs land with someone who can actually resolve them.

That’s the real shift. Those tough trade-off decisions that sat unresolved – or even unspoken – in middle management layers are now surfaced and can be acted on by someone with the cross-functional reach, time and CEO sponsorship to move quickly.

The early returns are tangible: wins in UI and GTM strategy (incorporating AI to attract attention and respond faster), plus longer-term projects to overhaul our onboarding UX and rewire how we pitch and win embedded partnerships.

So, how does this address fuzzy ownership? My hypothesis is that the CPO – and the broader product function – needs to evolve and take the lead in driving coherence.

Conversations with product peers show me we’re all feeling this pull (or push, if you’re not leaning into it). The smarter ones are concluding that the product function isn’t dead; it’s becoming the coherence function.

It’s still early days, and I’m learning as I go. But if I’m right, the best product leaders won’t be managing roadmaps – they’ll be the connective tissue holding the whole mission together. Let’s see if it holds.

The DAT premium party is mostly over. Since the November 2024 peak, over $60B has been wiped from DAT market caps. Nakamoto’s stock price crashed ~98%, now trading at a double digit discount below net asset value – the biggest failure to date. The market learned the hard way that holding someone else’s BTC isn’t worth a premium unless they’re doing something exceptional.

It’s not all doom and gloom though. Strategy’s (MSTR) capital innovation and XXI’s ecosystem investments still justify their valuations IMO. MSTR gives retail and institutional investors an “easy” path to discover Bitcoin, offering a range of instruments including yield. XXI has a worthy mission to be a full-fledged Bitcoin ecosystem. They’re worth a dabble with speculative capital, but don’t bet they’ll outperform just hodling BTC.

Beyond DATs, there’s a deeper problem: companies have failed to demonstrate that value flows back to L1s predictably. Lightning infrastructure is winning, but does routing revenue accrue to BTC holders? DeFi protocols move billions, yet LINK – the backbone oracle – has a chart that looks terrible despite obvious utility. At ETHDenver a few years ago I heard founders openly ask “Why do I need to pay Vitalik!?” They’re capturing value at their layer, not the base.

I’ve made these mistakes myself. Chased SUI (selling my SOL stack) thinking I was early on a better L1. Rotated my ETH bag into Bored Apes thinking blue-chip NFTs were the play. Still holding both – what I thought were quick wins turned into multi-year bags. Lost not just in dollars, but in BTC terms. The opportunity cost of not just stacking kills you twice.

So here’s where I’ve landed: My core holdings stay in BTC. Accept I’ll never have enough. Try to buy the dips. We’re still early.

But I’m not sitting out entirely. My speculative capital goes to the handful of companies I believe are genuinely strengthening Bitcoin’s L1 – not just building on it, but making Bitcoin itself more valuable and inevitable.

Bitwise is building the on-ramp infrastructure. Millions of retail investors get exposure through their funds. BTC remains their biggest AUM for a reason. Long game, but essential as adoption accelerates.

Voltage is tackling Lightning GTM better than anyone. If anyone can deliver a true Bitcoin L2 that works, it’s them. The ambition is there, and getting it right means BTC becomes a more usable medium of exchange.

Fold took a beating but made smart long-term choices – strengthened their cap structure, kept shipping their credit card, has multiple irons in the fire. They’re thinking in years, not quarters, and bring daily BTC utility to the masses.

The bar is higher now. We’re still building the plane while flying it, but I’ve never been more optimistic about Bitcoin’s future. There are no guarantees, of course. But, if you’re going to invest beyond pure HODLing, back the companies that make Bitcoin better, not just their own treasuries fatter.

This has been in my drafts for months and – somewhat depressingly – the topic is still around today. The thinking is that the economy moves in four year cycles and, perhaps more relevantly, Bitcoin price does too. We got our Q4 crash and bitcoin dipped ~50% with fear levels having been close to historic lows, and now we’re grinding or ranging depending on your viewpoint.

For four year cycle veterans this represents the “proof” that the cycle has ended and we are now in bear territory for months to come. For non four year cycle enthusiasts – aka “this time it’s different” bros – there are a dozen reasons for this blip and bitcoin is about to moon on a wave of liquidity the likes of which the developed world has never seen before.

So, who is correct, and does it really matter?

There is a real possibility both camps will be “right”. And, as the saying goes, everyone will get their bitcoin at the price they deserve.

Here’s what matters: from degen traders to Wall St, everyone’s trying to time the perfect entry. An investing framework might work for stocks or bonds, but bitcoin doesn’t care about your cycle theory. The opportunity isn’t in timing – it’s in not missing the accumulation window entirely.

The best time to buy the scarcest and hardest money ever invented was yesterday; the next best time is today. DCA if you need to smooth the entry, but don’t paper hand the opportunity to be early by waiting for a dip that may never come.

I used to think optionality (the ability to keep as many options available as possible) was a unique strength of mine.

This made me aloof and evasive on my position on many topics. The fear of offending somebody (and burning bridges) was real, and to some extent made sense when I was the least knowledgeable person in the room.

Once I had knowledge, however, an optionality preference meant that I was never convicted in my beliefs or actions. This made it easy to change my mind, but also eroded trust with people (professionally and personally) looking for decisiveness and reassurance.

The ability to change your mind is sacrosanct. The inability to make up your mind is cancerous.

Once I recognized this pattern in myself, I started seeing it everywhere. In leaders who hedge every decision through endless internal debate. In people (myself included) who stay quiet about their personal goals for fear of commitment or judgment. Preserving optionality feels safe, but it’s a slow leak of momentum and trust.

These days, I strive to lead with conviction and have confidence in my beliefs and actions until such time as new evidence presents itself.

This has created a snowball effect with my career, personal interests (focus on Bitcoin-led projects) and fitness goals (shredding and lifting my own body weight) where conviction builds on conviction and accelerates growth.

Being convicted also means saying no a lot of the time. A quick no – with a rational explanation – is way more effective most of the time than a long deliberation to preserve optionality.

Less time making decisions means more time working and building on what matters most.

Still a work in progress. I will change my mind a lot!

Bitcoin gave us a unique opportunity to think about things on a truly global, decentralized scale.

Most humans have some form of bias based on their geography and direct use case. Americans and Europeans (on the whole) are not bothered enough about debasement and payment frictions to care about crypto.

Bitcoin has found a more captive audience as a store of value and medium of exchange in countries with rampant inflation and capital controls. Think Venezuela, Turkey, etc. It is the ultimate form of currency that is independent of governments and institutions.

Emerging markets set the trend and developed markets follow. This is the reverse adoption curve for almost all existing products. As someone with experience developing global products it is still counterintuitive to establish PMF in small developing markets.

Stablecoins (I hope running on Bitcoin rails) are the first large (yet boring) use case that could be truly global in adoption. Most users care about being 24/7, fast and inexpensive more than they do about immutability, decentralization and security.

The more developed a market the more this is true.

Product builders need to make the case for the real benefits of blockchain technology (or not).

Personally, I care about the philosophy of Bitcoin, but there will be periods where getting a product into as many hands as possible is more important 📈

Current quantum tech can’t even crack factor-15 problems, let alone SHA-256. We’re talking orders of magnitude away.

The “secret quantum computer” theory doesn’t hold up. Given the public $Bs in quantum R&D, a similar shadow program would be nearly impossible to hide.

Here’s the kicker: Bitcoin devs aren’t quantum experts. BIPs are in progress, but nobody knows the real timeline or threat level.

Game theory matters too: even IF quantum breaks crypto, why target Bitcoin first? There are bigger fish (banking, military, etc). You’d get one shot before defenses mobilize.

The takeaway: Quantum concerns are real but years away. Bitdevs are moving deliberately, not panicking. Most current “quantum will kill Bitcoin” takes are FUD.

Nobody knows for certain. Stay informed, not anxious.

The title may be clickbait – tax isn’t a sexy topic – but nearly every BitcoinFi company building for institutions that I have spoken to sees it as a major barrier to entry. Tax obligations for Bitcoin and cryptoassets (since they are treated as property rather than currency in most jurisdictions) touch everything from payments to staking and lending. The elephant in the room is tax, and it remains a stubborn barrier to widespread adoption.

For individuals, it’s confusing and annoying. For institutions, the time dedication and compliance risks are several magnitudes higher. Internal tax teams worry about derivatives accounting, GAAP vs. IFRS treatment and quarterly mark-to-market requirements. I nearly had a major partnership deal unwind for exactly this reason! If the tax burden is not minimized, a tentative “Yes” can quickly become a hard “No” to the adoption of Bitcoin-led products.

The issue boils down to this: every movement of Bitcoin is a taxable event. While some countries have carved out narrow exemptions, the US and most OECD members have not. For BitcoinFi builders the table stakes are not just transparency (after all, this is an easy win for blockchain tech!), but robust infrastructure. This means reliable transaction data, technical attestations, audit rails and cost basis reconciliation, as well as API-led reporting that institutions can mold into their own views. These systems need to run 24/7/365 and feature excellent SDKs and templates with integrations directly into enterprise backbones like SAP and Oracle.

The crypto tax software market, worth $4.2B in 2024 and projected to exceed $10B by 2029, with a CAGR of 20%1, is mostly retail-driven today. Institutional needs are far greater, and the compliance burden in both time and money is likely to be 5-10X greater.

While it’s tempting to think stablecoins (fiat-denominated cryptocurrencies that effectively skip the tax issue because they are fiat pegged) are the solution2, I would argue these are inferior solutions that simply paper over the inconvenient tax treatment that Bitcoin suffers today.

Stablecoins appear to solve this by sidestepping capital gains calculations – and current adoption reflects that. Visa Onchain Analytics reported $8.5T in stablecoin transaction volume over the past 12 months3, compared with Bitcoin payments via Lightning which remain a tiny fraction of global settlement flows (optimistically estimated at 5%). But this is only a workaround. Stablecoins are inferior long-term and true adoption of Bitcoin is worth fighting for. The holy grail for BitcoinFi companies is simple: Bitcoin transactions should be recognized as currency movements, not taxable events.

Until then, progress will occur incrementally. A de minimis exemption for small payments (in current US proposals, under $2004) would remove friction for small day-to-day transactions. Global coordination of regulatory and legal requirements is also advancing, with the OECD’s Crypto-Asset Reporting Framework (CARF) set to standardize disclosure requirements across borders.

Meanwhile, staking (and/or wrapping) and lending of Bitcoin is more complicated. If a holder maintains custody of their Bitcoin it is generally not considered a taxable event, but wrapping it into another token often is (at least under US rules). Non-custodial staking is unlikely to be appealing to yield providers and lenders. Here lies a genuine design challenge for BitcoinFi companies.

The way forward is clear. Let’s be proactive while embracing the tax reality we currently have, build products that make compliance seamless, and keep lobbying for policy change. Best-in-class solutions will mean real-time cost basis reporting, the ability to export directly into tax forms, architecture that is ISO27001 and SOC2 compliant, and above all, integrations that make tax issues invisible to partners and auditors alike.

If Bitcoin is to power global settlement, we don’t just need 24/7 and cheaper rails. We need clarity and compliance – and the companies that deliver both will be the ones that succeed.

I want to talk about something potentially controversial – but timely – after spending a few days immersed in conversations at Bitcoin 2025 in Las Vegas.

We’re all Bitcoiners. I don’t need to convince you of bitcoin’s soundness or the uniqueness of the Bitcoin network. But I do want to explore how we can do more with our BTC. How to extract more utility from bitcoin beyond simply HODLing it as a store of value.

Many of us feel we’ve escaped fiat decay and taken control of our financial destiny. But in practice, we’re often left cash flow neutral (or worse) with assets we don’t want to sell, and limited ways to tap into their value.

So let’s talk about four approaches to increasing bitcoin’s utility:

Spending it

Buying bitcoin-adjacent instruments

Staking it to earn yield

Borrowing against it

The case for spending

Bitcoin’s store-of-value status is well earned, but its original purpose was as money. It says so in the very title of Satoshi’s infamous white paper: “A Peer-to-Peer Electronic Cash System.” Ignoring Bitcoin’s payment function risks weakening its potential as the future financial system.

The Lightning Network is the best (current) way to bring bitcoin’s payments vision to life. It enables instant, low-cost global transactions and is growing more robust by the day. I’ve been running a Lightning node for a while now, and while it’s taught me a ton, you don’t need to be a technical wizard to participate.

Even without running a node, you can use Lightning to send and receive bitcoin instantly, with better UX than many banking apps. (And, if you do venture into running your own Lightning node – and I highly recommend it – you can earn modest but real yield through routing fees if you manage channels efficiently.)

Look out for:

Cash Apphttps://cash.app/ | Possibly the slickest UX and on/off ramp for making payments with bitcoin.

Lightning Labshttps://lightning.engineering/ | Early mover offering a Layer 2 protocol for building Lightning-powered applications.

Lightsparkhttps://www.lightspark.com/ | Brainpower from the team behind Libra now focused on enabling institutions to scale Lightning payments.

Umbrelhttps://umbrel.com/ | An approachable way to run a Bitcoin+Lightning node with an active and helpful community.

The case for investing

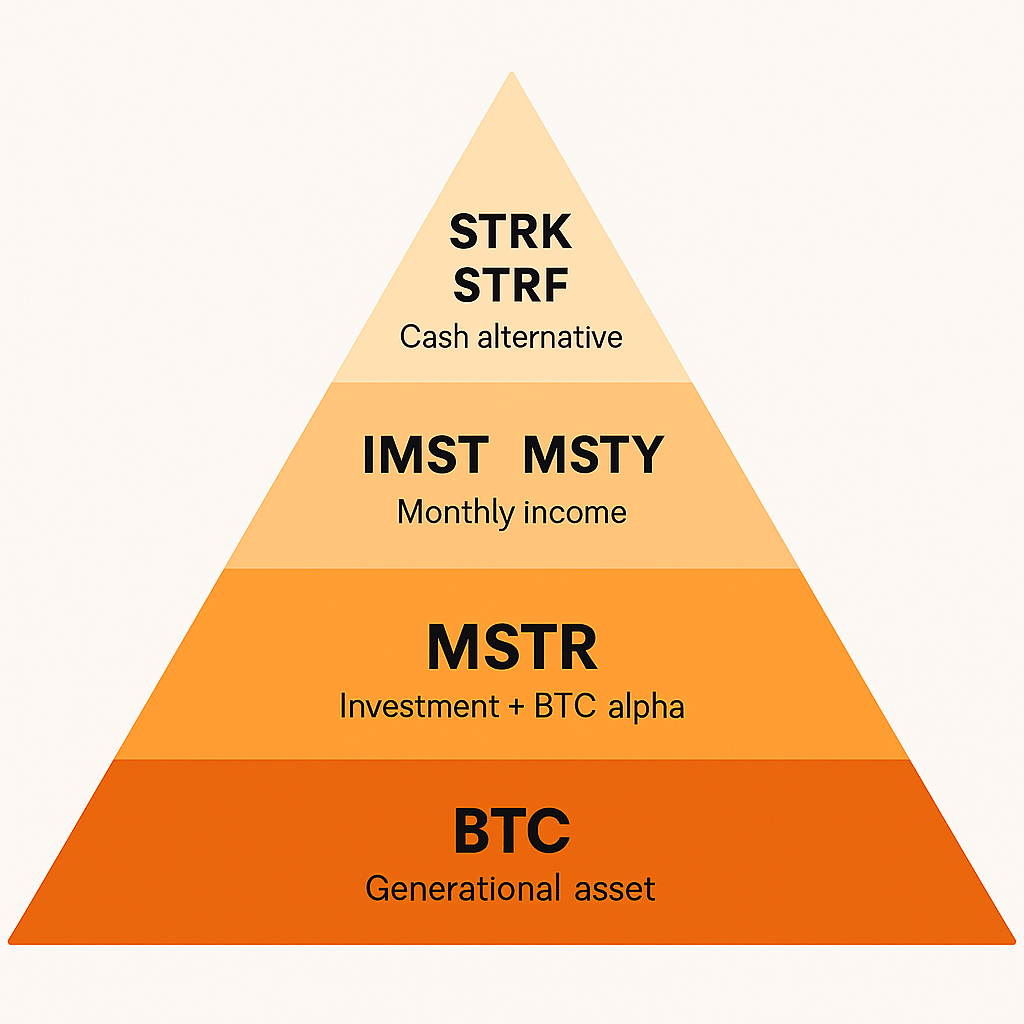

If you’re bullish on BTC’s long-term trajectory, you can express that view through exposure to bitcoin treasury companies or structured funds that track bitcoin performance – often with easier access and tax benefits if you invest in a pension or other efficient wrapper (DYOR, not financial advice).

Michael Saylor’s MicroStrategy ($MSTR) is the original Bitcoin proxy. But new contenders are now vying for the crown of the purest and most transparent bitcoin treasury company. Furthermore, products like $MSTY and $IMST have emerged to offer leveraged or derivative exposure, and $STRK or $STRF are pushing the idea of stable, income-oriented bitcoin-backed instruments even further.

I’m personally using MSTR options to speculate with limited capital at risk, but structured funds might be appealing for those seeking passive exposure or looking to diversify their existing portfolio.

Look out for:

Bitwisehttps://bitwiseinvestments.com/ | Leading crypto asset manager with thoughtfully designed products, bleeding-edge quants and a commitment to funding open-source development.

Strategyhttps://www.strategy.com/ | The OG Bitcoin treasury company. “There is no second best” – Michael Saylor.

Twenty Onehttps://xxi.money/ | Backed by Cantor Fitzgerald and Softbank, aiming to build the most transparent bitcoin fund yet.

The case for staking

This was the hot (over-hyped?) topic at Bitcoin 2025 – and also the most misunderstood.

Let’s be clear: staking bitcoin is not the same as staking in proof-of-stake systems like Ethereum. Bitcoin doesn’t have a native staking mechanism. So when a provider offers “bitcoin staking” what they really mean is: your bitcoin is being deployed in a strategy that generates yield, and they’ll share a portion with you.

This raises critical questions:

What is my BTC being used for?

Is it being lent out, wrapped, or used as collateral?

Who controls custody?

Is the yield sustainable – or subsidized?

One standout company building in this space is Acre. You deposit BTC and earn BTC, without needing to convert it into tokens or move off-platform. Behind the scenes, Acre uses secure and decentralized infrastructure to put your BTC to work, with yield coming from demand to rent liquidity for leverage – akin to an on-chain money market. It’s early days, but the design aligns incentives well and emphasizes transparency and user control.

TL;DR If you’re going to stake your BTC, make sure you understand the mechanics and the risks.

Look out for:

Acrehttps://acre.fi/ | Backed by Thesis. An on-Bitcoin yield protocol offering native BTC compounding to consumers and institutions.

The case for borrowing

This one almost needs no introduction. If you need cash but don’t want to sell your BTC, borrow against it. The idea is as old as finance itself – securing a loan with collateral – but Bitcoin makes it programmable.

The big concern here is rehypothecation: are your coins actually held 1:1, or are they being reused behind the scenes? Trust and transparency are key. There’s also market risk: you’re using leverage (true, even if it doesn’t feel like it!). If BTC drops, your loan may be liquidated unless you top up your collateral.

Ask yourself:

Can I support interest payments if my income drops?

What are the margin requirements and what happens if bitcoin’s value declines?

Who are the underlying capital providers, and in what circumstances can they exercise rights to my bitcoin?

Still, when done responsibly, this can be a tax-efficient way to fund fiat expenses – or buy more bitcoin – without selling your stack.

Look out for:

Mezohttps://mezo.org/ | Built by Thesis. Bitcoin-backed lending with a promised competitive borrowing rate. Mainnet was launched during Bitcoin 2025.

Strikehttps://strike.me/ | The Bitcoin financial products company that never fails to amaze with its ability to ship fast and delight users.

From HODL to Action

Bitcoin is pristine collateral. It’s hard money. It’s digital gold. But for Bitcoin to become the backbone of a new financial system, we need to use it, not just stack it.

Consider how spending, staking and borrowing and experimenting with bitcoin-adjacent products fit within your risk appetite. And let’s help the buidlers out there create a world where Bitcoin powers real economic activity – without compromising what makes it special.

A thought piece reflecting on a side degen project I ran in 2023 and a potential opportunity for a leading crypto fund manager. Just for fun. All thoughts and opinions expressed are my own.

NFTs [Non-Fungible Tokens] have served as a gateway into crypto for millions. Unlike many digital assets, NFTs don’t require deep technical knowledge to spark curiosity. The appeal of a Pudgy Penguin or an XCOPY 1:1 speaks for itself. Communities have formed around top collections, often delivering outsized returns to those fortunate enough to mint a genesis NFT.

Yet institutional-grade access remains limited. Bitwise was an early mover, launching its Blue-Chip NFT Index Fund in 2021, but there’s still no pathway for deeper, more dynamic exposure aligned with the true nature of this market.

A Strategic Fit for Bitwise

Bitwise was founded to provide clean, compliant and understandable access to digital assets. Applying a fund manager’s mindset to a tech-native domain, they’ve simplified access, reduced friction and built investor trust.

A managed NFT fund would be a natural extension of this approach. NFTs remain daunting even for established crypto investors, facing barriers around custody, pricing and trust. Bitwise has the brand, infrastructure and qualified distribution network to overcome these challenges once again – this time in the rapidly evolving world of Web3 culture and digital collectibles.

Such a fund would differentiate Bitwise strategically. Most institutional managers remain on the sidelines of NFTs, constrained by traditional valuation frameworks and benchmarking fears. Bitwise could step boldly into this space, reinforcing its innovative edge and potentially delivering outsized returns.

The Opportunity: Big, Underserved and Ripe for Structure

At its peak in 2022, NFT sales volume reached $23.7B (Cointelegraph). Although the market cooled in 2023-24, recovery is well underway. Projections estimate the NFT market will reach $35.7B in 2025 and expand to $211.7B by 2030 (Grand View Research), representing a CAGR of over 41%.

Recent high-profile sales illustrate renewed interest: CryptoPunk #3100 sold for $16M (4,500 ETH) and “Fidenza #313” by Tyler Hobbs went for over $3.3M. While these could be considered exceptional, these sales highlight the broader appeal and potential of digital collectibles.

Yet there’s no agreed definition of a “blue-chip” NFT. Even among crypto veterans, passionate disagreements persist. Factors like emotional resonance, historical significance and collector sentiment complicate traditional valuation frameworks.

In January 2025, respected NFT researcher/collector ‘Jediwolf’ attempted to rank the top 100,000 NFTs. Initial consensus quickly dissolved into debate, leading Jediwolf to conclude “some people will inevitably be dissatisfied and there’s little that can be done to appease everyone” (tweet). This highlights the complexity and emotional depth of NFT investing – a domain ripe for a structured, data-driven approach.

Bitwise could lead by developing a sophisticated model that blends cultural signals with on-chain data, offering investors diversified, real-time exposure to this opaque asset class.

A Personal Experiment: Building a Model

During summer 2023, I attempted to create such a model-driven fund. Friends frequently asked how to invest in NFTs, and I realized I lacked a definitive answer. I began developing a model focused on investing in top NFT collections and exiting based on multiples or market indicators.

Working with Dune Analytics, I analyzed NFT trading pairs – items with observable buy/sell history – organized by collection, rarity traits and historical performance. However, extensive wash trading and bot activity obscured meaningful data, and the rapid emergence of NFTs on new chains (Bitcoin Ordinals, Solana’s Mad Lads, to name only two) quickly outdated my initial models. Continuous updates were clearly necessary, though the concept itself remained sound.

Beyond investor returns, such analytics could also benefit custodians, insurers, and digital and physical auction houses. These stakeholders could contribute to model insights, offsetting operational costs and amplifying industry interest.

Additionally, NFTs often offer utility such as event access, pre-mints, or airdrops – benefits that fund investors could directly enjoy, providing tangible value beyond price appreciation.

Challenges (and Why Bitwise Is Better Equipped)

Despite initial enthusiasm, my project stalled due to the required upfront capital, regulatory uncertainty and limited short-term returns. Investors showed intrigue, but hesitated without institutional backing. I shelved the idea, until a chance encounter at a recent crypto event brought it back to mind.

Bitwise – unlike individual entrepreneurs – possesses the infrastructure, trust and regulatory expertise needed. Still, risks remain significant. NFTs carry reputational and emotional weight – one controversy can rapidly depress floor prices.

Practical questions also persist: What regulatory jurisdiction will the fund choose, and how will it affect investor eligibility? What rights will investors have over the NFTs? Issues around intellectual property, usage, airdrops, and perks must be addressed transparently.

Liquidity also poses a challenge. Unlike most Bitwise products, NFTs from top collections often lack immediate market liquidity. Clear communication regarding lockups, redemption terms and valuation will be essential, though liquidity should naturally evolve as the market matures.

Time to Go Beyond the Basics

Bitwise’s existing Blue-Chip NFT Index Fund, based on quarterly rebalancing, was appropriate in the market’s early days. Today’s NFT ecosystem demands more sophisticated, data-informed models capable of capturing real-time nuances. Get this right and the potential is enormous!

A Next Frontier

Launching a managed NFT fund aligns perfectly with Bitwise’s mission of democratizing crypto investing. Leveraging its strengths – education, compliance, trust – Bitwise could confidently pioneer this next frontier in digital assets.

The following text is part of a summer 2022 research piece that has been reproduced with kind permission of co-author Porter Orr.

How do Platform Companies think about Data Sharing and how does this inform their Organic vs. Partnership Growth Strategy?

Abstract

While this analysis mainly focused on US companies – such as Amazon, Shopify, Square and Stripe – and their activities, the conclusions summarized herein can be applied more broadly and are especially relevant for non-US companies looking to break into North America. The authors note upfront three key takeaways from this research:

Product companies need to commit to fully migrate to a platform company mindset to benefit from network effects.

The perception and reality of trust are very clear to consumers. If correctly exploited, network effects can exponentially grow marketplace value, but they work both ways when trust is eroded. Consistency is therefore key.

A successful platform company not only solves problems for its users, but continuously captures and uses data to create new complements.

Open and fair marketplaces that merge data and lean into third party developers are likely to be the most successful in creating long-term value.

The most successful platform companies lean into third party developers to solve problems that are not aligned to their core capabilities. This enables the value of the marketplace to be greater than the sum of its parts.

Merging new sources of data is ethically sound if done for the benefit of your users, often uncovering new problems unknown to your customers.

Open and fair marketplaces have endured and continue to create long term value most effectively. In well managed marketplaces, this does not necessarily prevent the platform company competing directly with partners.

In North America ethics and trust are especially important. The upsides and downsides are likely to be significantly enhanced compared to existing core markets.

Merging data is commonplace in North America. This is table stakes to simply compete with incumbent platforms.

Companies must maintain a high ethical bar that is never ignored for short term gain. This requires incredible discipline, but is worth it.

The core part of this analysis is broken into three sections:

Product vs. Platform Mindset, Trust and a System Dynamics View

Key Takeaways of how Successful Platforms Operate with Data

What Strategic Considerations Exist for US Competitors?

What is a ‘Platform’?

For the purpose of this analysis, we chose to use the definition provided by Bill Gates1, namely: “A platform is when the economic value of everybody that uses it, exceeds the value of the company that creates it.”

We also leaned into the concepts provided within McAfee and Brynjolfsson’s epic book ‘Machine, Platform, Crowd‘ regarding the general features that platforms employ:

Complements – Provide numerous solutions which are adjacent to the core product.

Superior UI/UX– User interfaces (UI) and user experiences (UX) that are top-tier.

Network Effects – Harness the power of network dynamics which systematically reenforce growth of demand, especially in two-sided or multi-sided marketplaces.

Unbundling and Rebundling – Dissecting or combining products and/or features, resulting in ability to serve unique and niche customer problems at scale.

Rapid Combinatorial Innovation – Continuous innovation of novel solutions is empowered with insight from an ever-increasing wealth of data, then often solved by combining existing platform capabilities in new ways.

Platform Stacks – Platforms are often built on other platforms, which harness network effects not only to further drive demand, but also increase breadth and depth of the solution provider.

High Switching Costs – When designed well, end users and partners usually have significant barriers when considering a change to another solution.

We further define a Core Offering to be the main product with which a company started. In-house complements are additional solutions that are now provided on the platform, which are internally branded. Marketplace complements are additional solutions which have been built on top of the platform by third party developers.

Product vs. Platform Mindset, Trust and a System Dynamics View

Moving from closed to open.

There is a subtle shift that is required for a company that is growing from a product based company to a platform company. For a product company, the goal is to maximize user value by developing the best solution to the users’ problems. For a platform company, the goal is to maximize user value, however the method of how to deliver that solution may vary. As the breadth of complements expands away from the core product offering, the platform company may build, partner, acquire, or otherwise depend on a third party marketplace offering.

The most effective platform companies embrace this shift to create an organizational culture that reinforces this new open mindset.

The imperative of building and maintaining trust.

In addition to embracing this open mindset, platform companies need to build and maintain trust with all user groups and be aware of the risk they face when violating that trust. When the gap between what a company advertises and what it actually practices widens, so does the probability of trust erosion. If trust degrades, then the activity of all user groups (customers, developers, and partners) will decrease, directly affecting both short term and long term value. As a result, platform companies risk more when violating trust than product companies, because the effect is amplified across all user groups at the same time.

Simply put, the network effects that help platform companies grow rapidly can also make them shrink rapidly if trust is violated.

Platform company successes hinge on core data insights.

A product company typically views its long term success by how well it solves a problem for a customer. The better the solution, the more likely the customer is to buy it. The data the product generates helps the company understand what features to add or improve on the core product.

By comparison, a platform company views success on two metrics: (i) how well a solution solves a given problem, and (ii) how well it uses the data generated to create new complementary solutions. Thus, for a platform company, data is not just used to improve a core product offering, but also to grow the entire platform. This directly drives the platform’s main purpose of creating value for all users that exceeds the value captured by the product company.

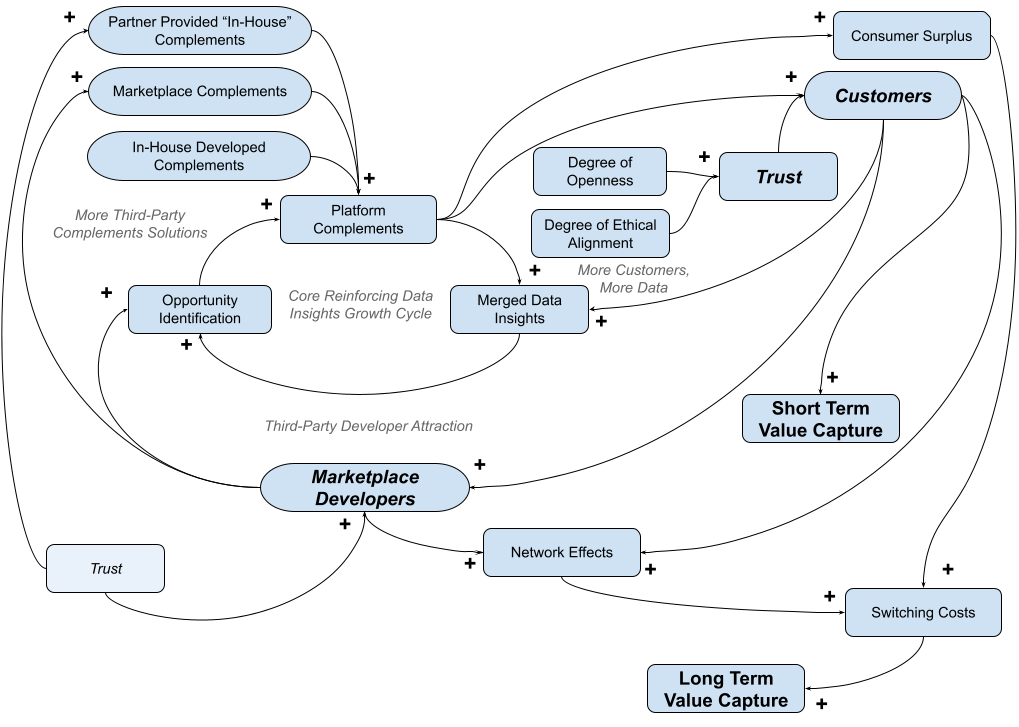

Platforms – A system dynamics perspective.

To help understand a platform system and its relationships, see the below visual map.

At the core is the ‘reinforcing data insights growth cycle’, a reinforcing cycle that begins as new complements are added and their data streams merged. As data insights increase this drives an increase in opportunity identification and developments that create even more complements and data. In addition, the model adds ‘degree of openness’ and ‘degree of ethical alignment’, both of which directly influence trust and authenticity. As a result, the diagram shows the effect these three components have on creating both short and long term value.

Figure 1 – System Dynamics view of Platform

System Dynamics Note: In the above system map, a ‘+’ indicates the correlation between two variables. In other words, if ‘Platform Complements’ increases, then ‘Merged Data Insights’ increases. In addition, if ‘Platform Complements’ decreases, then ‘Merged Data Insights’ decreases. Additionally, there are several reinforcing loops, such as ‘Core Reinforcing Data Insights Growth Cycle’. These loops create ‘flywheels’ that can either help or hurt the company depending on the directions of the variables that create the loop as they either grow or shrink.

Key Takeaways of how Successful Platforms Operate with Data

Maximize customer value by implementing the best solution to drive data generation.

As Figure 1 depicts, the core of a platform company’s success hinges on creating complementary solutions that solve a wide array of problems for customers. By providing superior solutions, more customers will adopt the solution.

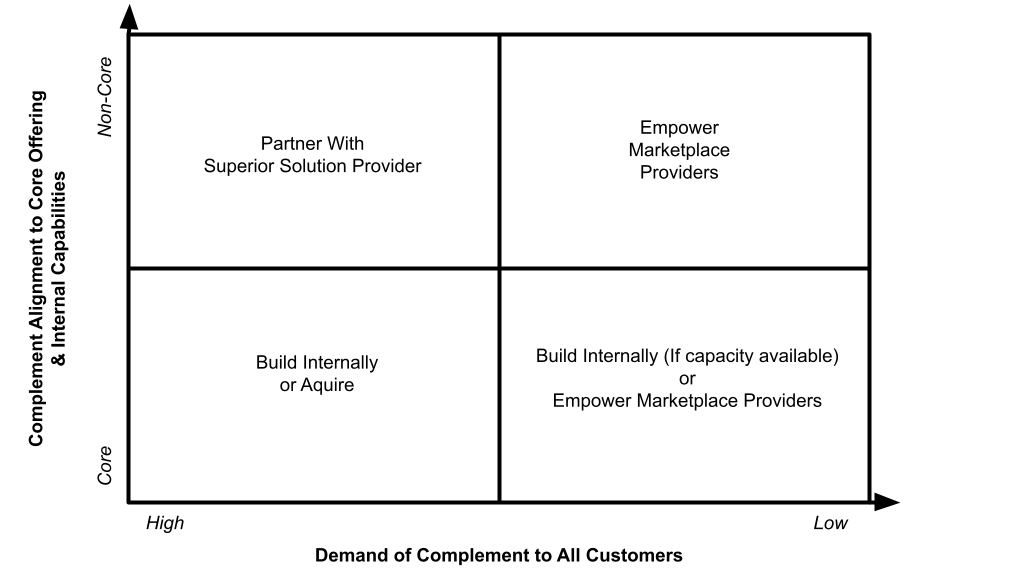

As the knowledge and experience of platforms has evolved over the past 10+ years, so too have the methods to grow a platform. In the past, companies aimed at building all in-house complements themselves (or acquiring them), then providing a marketplace. Doing so enabled short-term revenue maximization by capturing all marginal profit. However, as the number of superior platforms have grown, some companies have shifted their strategies on when to build internally, when to partner, and when to outsource to the marketplace. The below diagram provides a framework for this.

Figure 2 – When to Build, Partner or Outsource to Marketplace

As depicted in Figure 2, in today’s marketplace, wise companies wishing to implement and maintain a platform are willing to outsource to a strategic partner complements that are in high demand for platform customers, but are not highly aligned to the platform company’s core set of capabilities.

Pursuing this strategy enables the platform company to:

Provide the best possible solution to their customers, which drives growth and consumer surplus.

Decrease the time and cost to market, and ongoing maintenance costs.

Reduce the ongoing operational cost of maintaining their own competing solution, and doubling down on what they do best.

Maintain a forward leaning brand image with customers staying within its ecosystem.

Gather and merge all data for the benefit of the users.

Effective platform companies understand the importance of cohesive data, and use it for the right ethical reasons. As superior complements are added, the data they generate increases two fold. First, any complement pulls in new types of data provided through its functionality. Second, the volume of customers using the complement increases, because they are superior in performance to other substitutes.

Successful platform companies combine these various data streams to gather the most cohesive understanding they can of the customer. This insight then enables the platform company to mine for new, previously unknown, problems; often, these are problems that customers might not even know they had. Then, either using existing complement or partner functionalities, the platform company can use combinatorial innovation to quickly solve the problem and offer a solution to their customers.

Key is the willingness of the platform company to merge various data streams, but doing so for the right ethical reason. Effective platform companies see the purpose of blending data is to help their customers.

Maintain a fair marketplace to generate secondary solutions with rich platform data.

The most successful platform companies that employ marketplaces do so openly and fairly. By providing access to a rich source of platform data, developers can also create secondary solutions that further increase the demand of the entire platform. Moreover, well managed platforms also seek to align incentives with the developer, providing mutually beneficial terms, revenue sharing agreements, and operational practices. In addition, experienced platform companies try to minimize the copying of existing solutions on their marketplace. If they do choose to compete with a third party complement, they do so openly and fairly, marketing their in-house solution on level terms with the solution of the third party developer.

Operating a marketplace with this mindset shows a level of platform economic savvy which maximizes long term value capture for the customer, developer, and platform company.

Companies with unique data have significant leverage as regulation and progression open up sectors such a financial services.

In a world of Open Banking (as one contemporary example) massive datasets will begin to commoditize access to, and the insights derived from, financial data. With rapid growth of Open Banking data, many entrepreneurs have begun to build and offer solutions that are highly attractive to customers. Many of these customers may overlap with the platform company’s user base. To compete, platform companies need to look towards the strength of their core offering. Platform companies with an existing, unique data set hold significant value and attractiveness to these new up and coming Open Banking empowered start-ups as a solution to partner or integrate with.

What Strategic Considerations Exist for US Companies?

Embrace merging and using data from users for users.

A high ethical standard of data usage will be key to the long term success of any company’s expansion within the US. This might sound like a contradiction – or even form a potential ethical barrier – against merging data streams from core products and complements.

This should not be the case. In fact, customers that already trust a company to manage their data securely and privately also desire ever improving products and complements. They desire value. The only way to deliver well on these improvements and growth opportunities is to merge data. In fact, for a newcomer to compete effectively in the US against incumbents and other platform providers in adjacent markets, it is essential. It is table stakes and not doing so would likely mean less informed product capabilities, reduced complements growth, and lower customer adoption over time.

Ethical redline considerations.

A strong commitment to ethical behavior and practices, especially as it relates to data and privacy, can be a differentiator vis-à-vis other large enterprises. It is, however, imperative for a company to stick to these commitments, to ensure trust with all users of the platform does not erode. This might mean making short term revenue sacrifices, or possibly taking an unpopular stance on contentious issues, as Apple famously did when requested by the Federal Bureau of Investigation to circumvent its own device security measures3.

There has been no point in North American history where trust in institutions has eroded faster than it has over the past several years. The costs for violating this trust is massive for companies when they find themselves on the wrong side of the fence. Meta with the Cambridge Analytica4 scandal, Uber5 and the Me Too Movement6, systemic racial inequality across many enterprises, all means maintaining trust with customers has never been so difficult, or so critical.